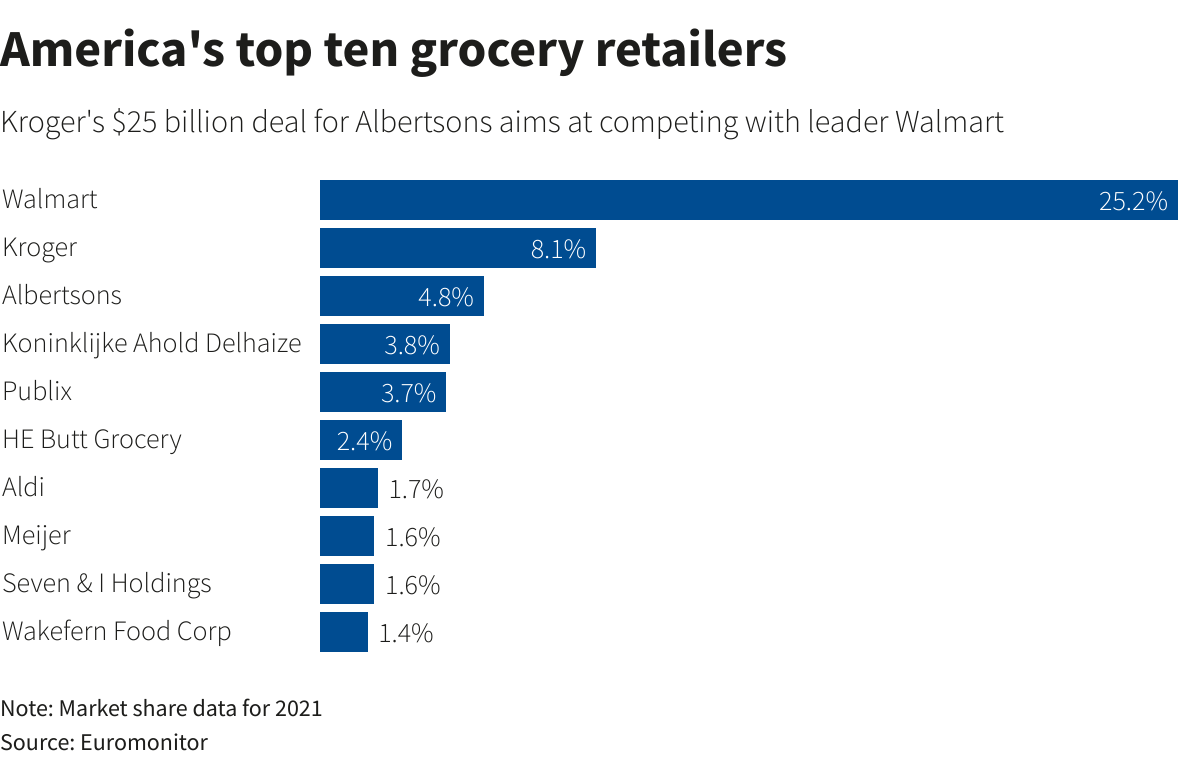

On October 14, Kroger announced plans to acquire Albertsons for a fee of $24.6 Billion ($34.10 a share) , a potential game changer for the grocery market. Combined, the companies would have an annual revenue of $209 Billion and operate over 5000 stores nationwide. The pro forma company would come close to rivaling Walmart, falling only $10 Billion in annual revenue short to the grocery behemoth.

The deal is expected to face a heavy test in passing regulatory authorities—with prominent members of both parties calling for its rejection. The announcement spawned trust-busting sentiments from both Bernie Sanders (D – VT) and Mike Lee (R – UT), both citing the recent rise in food prices (11 percent YOY) and the potential for the new conglomerate to exacerbate the issue facing Americans’ pocketbooks.

In order to potentially mitigate these concerns, the pro forma company would consider spinning off up to 375 stores into their own separate company, although even this may not be sufficient to pass Federal Trade Commission (FTC) authority. If approved, the move could lead to a major change in the grocery landscape—directly impacting the everyday lives of millions of Americans. The ultimate question is: will the benefits to business outweigh the potential risks to grocery prices?

Goldman Sachs and Credit Suisse were the primary advisers to Albertsons while CitiGroup and Wells Fargo advised Krogers in addition to arranging $17.4 Billion of debt financing to support the deal. The deal dictates that Kroger pay Albertsons $600 million upon termination.

Be First to Comment