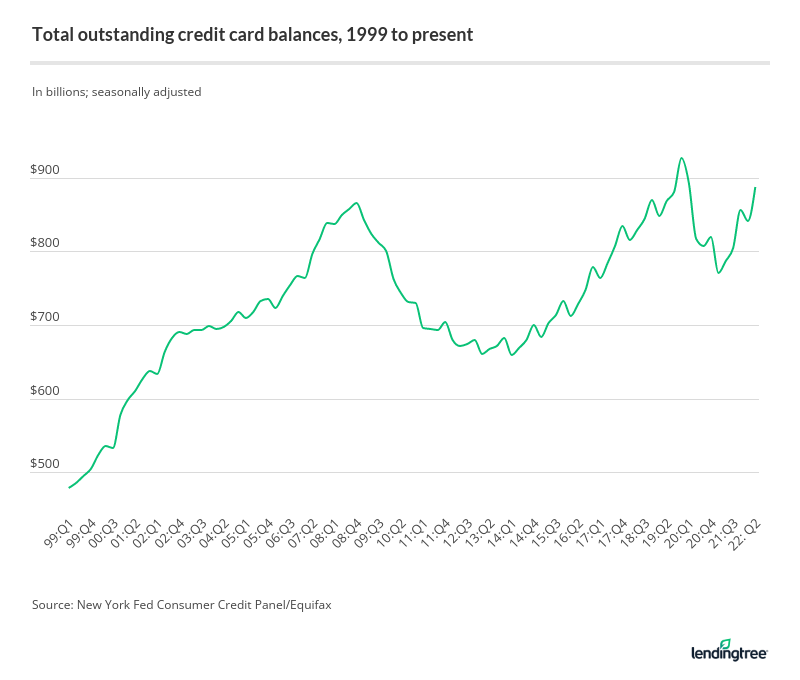

What could $887 billion get you? It could buy you the Denver Broncos about 180 times over, all of Tesla’s enterprise value, or about 2000 of the world’s nicest superyachts if that floats your boat. As much as we can wish that $887 billion were representing an exhilarating potential acquisition or new industry investment, it is instead the total credit card debt of Americans in 2022.

While this number in and of itself might be startling, consider the invisible cost of credit card debt: massive APR. For new credit cards, the average APR in Q2 of 2022 was 15.13%. For reference, this is about 5% higher than Warren Buffet’s returns for the last 20 years. When pairing these high APRs with the extended periods of time that Americans tend to carry this debt, trouble appears on the horizon.

The story does not end with the sheer volume of debt, but rather, it extends to the impact that this debt has on many consumers through the effect on their credit scores. That debt figure is one of—if not the—most impactful aspects on your credit score. Along with running over your limit is running too close to your limit. The general rule of thumb is about 30% of available, so if one were to have $5000 in available line per month, then 1500 showing up on the statement date would be a safe amount.

So why do we care about credit scores? A credit score is amongst the most important numbers in life—along with your birthday, social security number, and now phone password.

One of the most impactful aspects of credit is when applying for mortgages. A difference in score can add up to hundreds of thousands of dollars in additional money spent or saved. Another prominent way is the application for new lines of credit with a lower APR, higher cashbacks, or more benefits (such as miles, etc.).

Finally and perhaps most important for every student reading this is refinancing student loans. When it comes time to pay these loans off, many opt to pay off their government or higher-rate student loan with a lower-rate personal loan if found eligible. The credit score that one has heavily affects those rates offered, which ultimately dictates the amount of savings that one is (potentially) able to enjoy.

So how can I fix my credit? First and foremost, avoid damaging it in the first place. It may go without saying, but one of the most important lessons a young adult can learn is the importance of maintaining proper credit, spending, and saving habits. Next on the list is, of course, making your payments on time for 6 months minimum. This demonstrates a habit of good spending and responsible credit (thus making lending companies view you as a less volatile lending target). Also, avoid opening useless lines of credit with online retailers. Be smart in searching for your credit cards (more on that here).

Overall, establishing credit is incredibly important. Do not let those huge debt figures scare you away from giving yourself a very solid leg up in life by beginning to build good credit at a young age. Credit, like most things in life, can be a beautiful asset if done properly and safely.

Be First to Comment